Best mobile banking features: What to look for in your banking app

Key takeaways

- Mobile banking apps now offer AI-powered financial insights, biometric security, real-time fraud detection and automated savings tools beyond basic account access.

- 86 percent of consumers use their banking app weekly in 2025, making mobile features a crucial factor in choosing a bank.

- When selecting an app, prioritize security features, user experience and financial management tools that align with your specific goals.

If you still think mobile banking apps are primarily for checking balances and depositing checks, it’s time for an update. Today’s best bank apps offer features that can fundamentally transform how you manage your finances, from AI-powered spending insights to automated savings tools.

Here’s what you need to know about what you can get from a mobile bank app today, and what to expect next.

Mobile banking statistics

- 55 percent of consumers report that using a mobile device is their top option for managing their bank accounts. (American Bankers Association)

- 64 percent of Gen Zers (64 percent) and 68 percent of Millennials use mobile banking apps most often (American Bankers Association). The use of bank tellers as the primary method of account access — which has been on the decline — is more prevalent among lower-income and less-educated households. (FDIC)

Most important mobile banking features to prioritize

Security and authentification

Mobile banking security features have become significantly more sophisticated, incorporating multiple layers of protection to safeguard users’ financial data and transactions:

-

Biometric authentication has evolved beyond simple fingerprint scanning to include facial recognition, voice verification, and multi-modal authentication that combines several identifiers for enhanced security.

-

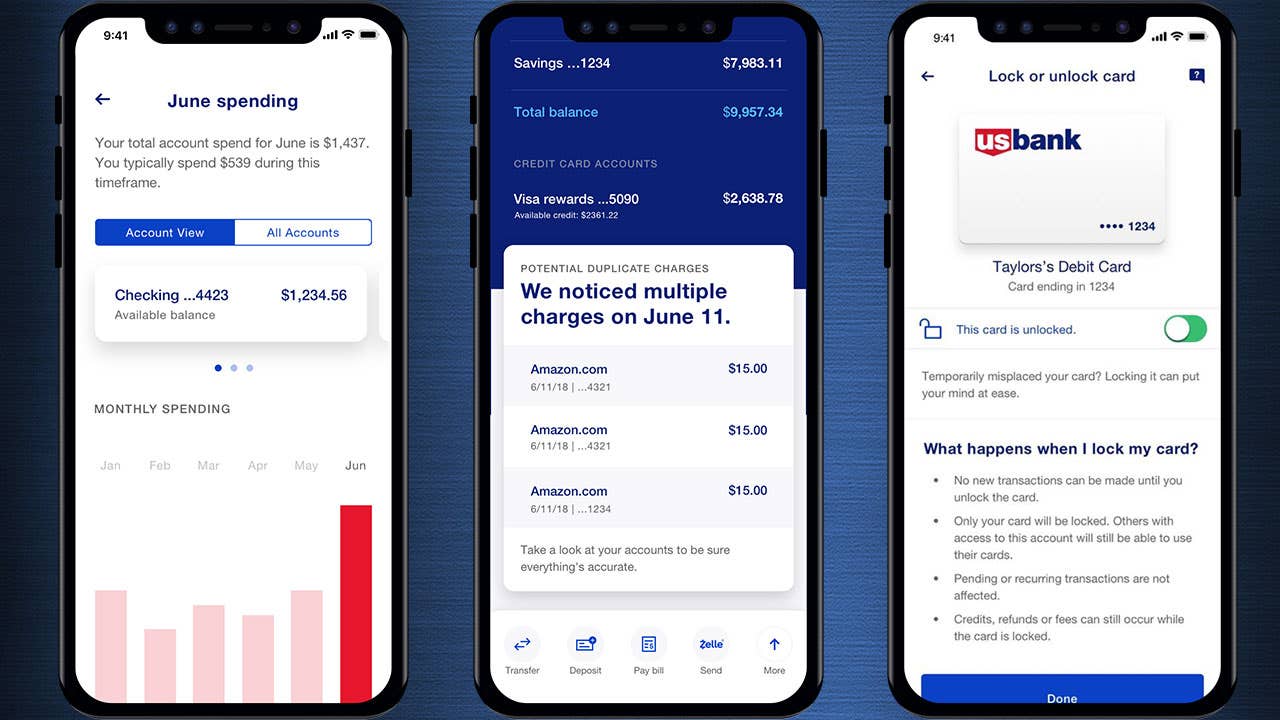

Real-time fraud protection has become more proactive and user-controlled. Many banks also offer AI-powered fraud detection that identifies unusual patterns and potential threats before transactions are even completed. Some may offer customizable security alerts that allow users to set notification preferences for different transaction types and amounts.

-

Card control features give users granular control over their accounts. This includes instant card freeze/unfreeze capabilities, spending limits by merchant category or time period or transaction-specific controls for enhanced security.

- Data privacy controls let you see which third parties access your financial data. Bank of America’s app, for example, shows customers exactly who has data access through their Security Center.

AI-powered financial management

Many mobile banking apps today have evolved into complete financial management platforms, offering tools that were once available only through specialized budgeting software.

In Bankrate’s recent emergency savings report, only 46% of U.S. adults have enough emergency savings to cover three months of expenses. Many consumers are struggling to stay on top of their finances and avoid going into more debt.

Banks are increasingly building features to help Americans save more and understand their spending habits:

Budgeting and tracking tools have become more intuitive and actionable. This includes features such as automated spending reports with customizable time periods and categories.

Bill management features have expanded beyond simple reminders. Some apps now include bill negotiation services that help identify opportunities to lower recurring expenses, and alert you when subscription costs increase unexpectedly.

For example, Huntington Bank launched a digital banking feature called Heads Up that predicts what a customer can afford to spend, when a merchant mistakenly double charges your card and more. Bank of America’s virtual assistant, Erica, now flags customers when a recurring charge or membership fee increases.

Digital wallet integration integrations

Digital wallets are increasingly becoming a norm as more retailers adopt cashless payment methods. According to a recent survey from Banked, almost 60 percent of consumers have used a digital wallet in the past month.

Mobile wallet features now extend beyond basic transactions to allow users to control multiple digital payment options from one interface, earn rewards on their transactions or use a virtual card for secure online purchases with temporary card numbers.

Some common examples of digital wallets include:

- Apple Pay: Available for Apple devices, Apple Pay allows users to make contactless payments within apps, stores or online by linking credit or debit cards.

- Google Pay: Similarly, Google Pay allows for contactless payments, but it’s compatible with Android devices and can be integrated with Google services.

- Zelle: Zelle is included in over 2,000 banks’ mobile apps as a way for individuals to send money to one another, directly from bank account to bank account. Check out our guide to using Zelle.

- PayPal: PayPal allows users to link bank accounts, credit/debit cards and even store money within a PayPal account. It supports online payments, money transfers and serves as a payment option for many online stores.

While many popular digital wallets aren’t directly provided by banks, banks can make digital wallets more accessible for consumers by making their bank accounts compatible with digital wallets or even integrating third-party services into mobile banking apps.

While digital wallets make it a lot easier to pay for things, they also potentially make it easier to get scammed. In many cases, you only need a phone number or email to verify who you’re sending money to, so make sure you only send money and make payments to trusted recipients.

Automated savings features

A number of banks are now offering mobile tools that can help you save through automated savings features, designed to remove the need for users to actively manage their savings. These tools automatically transfer money from one deposit account to another — typically from checking into savings — based on pre-set rules or algorithms.

Ally Bank’s app, for example, has a Surprise Savings feature that analyzes your checking account and spending history and automatically transfers a specified amount that it deems safe-to-save into a high-yield savings account.

Other banking apps, such as Varo Bank, boost savings by rounding up change from transactions and moving that amount into a savings account. Varo’s app also allows customers to choose a percentage of their direct deposit to be moved into their savings account each month.

Some banks are also using gamification to encourage users to save more consistently. These challenges often include setting specific savings goals, such as saving a certain amount by a set date, and rewarding users with badges, process tracking and even cash or APY incentives once they reach those milestones.

LendingClub Bank’s LevelUp Savings account serves as an example, rewarding savers with a substantially higher APY on statement cycles when they deposit at least $250 into the account.

Rewards and loyalty programs

Banking apps have evolved to help users maximize the value they receive for using their debit and credit cards.

Bank of America, for example, now offers a whole platform within its mobile app dedicated to cash back rewards called BankAmeriDeals. In the app, users can browse through all the stores and deals that are eligible for cash back rewards when they pay with a BofA debit or credit card.

That makes it easy for customers to quickly look at what rewards they’re eligible for when they’re already out and about shopping, so they can maximize their cash back. The app also lets users view all of the cash back rewards they’ve earned.

Other banks may offer points that are earned when you spend on certain purchases, which can be redeemed in a mobile app. U.S. Bank is one bank that’s made it easy for customers to redeem points whenever and wherever they like. Customers simply open the bank’s mobile app and can navigate to a rewards tab, where points can be redeemed for credit, merchandise, gift cards, travel and more.

How to choose the best mobile banking app

When choosing the best mobile banking app, it’s important to consider your personal financial needs and preferences.

As a start, search for an app that offers the core banking features you need, like the ability to transfer funds and mobile check deposit.

Security features should also be your primary consideration. Look for banks that offer multiple authentication options, including biometrics. Verify the bank’s encryption standards and data protection policies and check if the app offers customizable security settings and alerts.

From there, consider other factors that are important to you:

- User experience and interface

- Transaction options and limits

- Financial management tools

- Customer support options

A mobile banking app ultimately is akin to having a real-time view of your account. Think of the app as part of the range of services and benefits that the financial firm provides. Some firms do a better job than others with their apps. Ask yourself, does the app do what you need it to do? Does it provide you with the functionality that you desire? This could include real-time alerts and the ability to get a quick look at transactions, balances and payments.— Mark Hamrick, senior economic analyst at Bankrate

What’s next in mobile banking?

Expect your mobile banking app to only get better at helping you handle your money as banks form new partnerships with fintechs and make even more improvements to their apps.

J.D. Power’s most recent U.S. Banking Mobile App Satisfaction study found that peer-to-peer payments and virtual assistance gained traction with younger customers. Still, the study found that there is a great deal of variability among apps when it comes to personal finance management.

Another noticeable gap in mobile banking is that it’s not accessible to everyone. The FDIC’s How America Banks survey found that households with higher incomes, as well as those with higher education credentials, are more likely to use mobile banking. Banking technology may evolve to address the needs of those who don’t have as much income or access to mobile banking tools.

It’s a vast playing field out there — every bank’s app offers its own variation of features. A bank’s mobile app features can influence where someone decides to bank, since these apps have become closely tied to helping you save and managing your money.

The best mobile banking apps offer far more than basic account access — they provide features that can help improve your financial health through advanced security, personalized insights and automated tools.

When picking a mobile banking app, prioritize features that align with your specific financial goals and habits. If building savings is your primary concern, focus on apps with goal-setting and automation tools. If security is most important, look for multi-layered authentication options and fraud protection.

Why we ask for feedback Your feedback helps us improve our content and services. It takes less than a minute to complete.

Your responses are anonymous and will only be used for improving our website.